Ralph

Moss Limited

Ralph

Moss Limited

Click on graph for a larger image

Click on graph for a larger image

Being

prepared can help you see beyond temporary dips in mutual fund values

The low-interest-rate environment of the 1990's has spawned a new breed

of investor--hungry for higher returns and looking for them in the mutual funds.

As

yields on interest-earnings securities declined over the past several years,

investors turned in droves to mutual funds. Based on figures compiled by the

Investment Funds Institute of Canada, investment in mutual funds exploded to

almost $1.50 billion at the end of 1995 from $34 billion in 1990.

It's

true that mutual funds have potential for higher growth. But if you're new to

the game, brace yourself: Unlike Guaranteed Investment Certificates (GICs) and

Canada Savings Bonds (CSBs), the value of your mutual fund investment is not

guaranteed.

Sooner or later, most mutual funds will experience a

temporary downturn in unit value.

Your first step is to acknowledge the relationship between risk and reward. Highly secure investments, like money market funds, are reliable, but the returns are tied to current interest rates. If you're looking for better performance, you'll have to accept more risk by investing n bond and equity funds. While bonds and equities are more volatile, over the long term, they provide superior returns.

Successful fund strategies

Here are some guidelines to help you weather the inevitable market downturns.

Know how your investments behave. Knowing the potential

volatility of your funds--that is, how much they fluctuate in value in the

shorter term--will help you maintain your perspective during a performance

crunch.

Look at the fund's average annual compound return over five

years or more. This figure will help you compare returns of different mutual

funds. Then, check the year-over-year returns to give you an idea of

volatility.

In addition, always read the fund's prospectus for

information. It will outline the fund manager's investment style and clearly

identify the potential risks involved.

Assess the amount of risk you

are comfortable with. If you cannot bear the thought of your hard--earned cash

going into an investment that might go down in value--even it is means you could

make a substantial profit over the long term--stick with guaranteed or low-risk

investments like money market funds, GIC's or CSB's.

If the prospect

or market fluctuation doesn't alarm you, and you're patient, consider devoting

part of your portfolio to investments that are geared for growth. Know yourself

and know what your's getting into. Your financial advisor can help.

Diversify your investments. Spreading the risk means

picking a variety of investment types.

Even if you have a high risk

tolerance, for example, it's not wise to place all your money in aggressive

investments. Holding a variety helps to protect your portfolio from declines.

While one type of fund declines, other funds could be growing.

Getting

professional advise to tailor a diversification plan for you is a good

investment.

Take a long-term approach. The longer your time frames, the better chance you give your investments to perform to their potential. As noted above, equity mutual funds have historically earned more than interest-paying securities. However, over short periods, they are usually more volatile. The key to success for these funds is to focus on the long term.

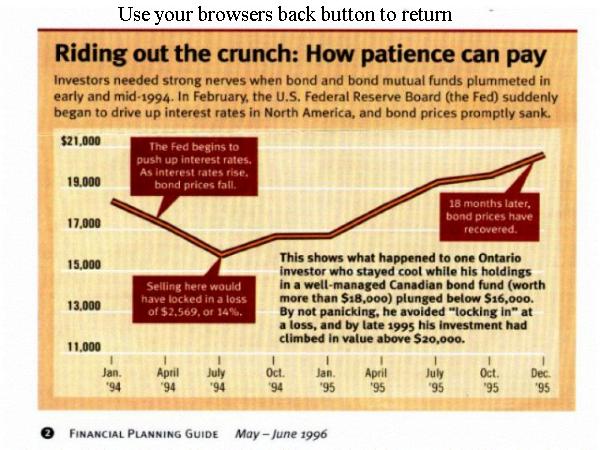

Don't panic. Don't sell just because your unit values decline. As the example below shows, chances are that the unit value will turn up again. If you bail out at the bottom, you're locking in losses, and missing out on potential future profits.

Don't jump from fund to fund. Many investors are

prompted to change their portfolio on the basis of unusually strong one-year

returns in another fund or another type of investment. Last year's winner isn't

necessarily going to be next year's top performer. If you're always chasing

last year's winner, you'll always be a year behind. Instead, focus on

high-qualify funds whose objectives match your own.

Before you

invest your money in mutual funds, do your research, and consult a financial

advisor. Be prepared to enjoy the market uptrends, and to wait out the

inevitable declines. In the end, if you've chosen wisely and monitor your

investments regularly, they should grow to their potential.

![[ARIAD]](../../ariadhomes2.gif)

![[HOME]](../../homebr2.jpg)

![[Email]](../../mailbr2.jpg)